In any case, I have seen quite a lot of complaining about it from industrialists, even to the point of threatening to unsubscribe. I find this ludicrous, at this point anyway. And here is why. The basis of much of the complaining is that people want to do their industry in highsec, and they believe they are being "forced" out to null. But so far as we know, this is not true. What is true is that industry "slots" are going away; instead there will be surcharges at busy stations. The surcharges are from 0-14%: "Expect costs ranging from 0% to 14% of the base item being produced for the most extreme case." (emphasis theirs).

People seem to be looking at the high end 14%, the "most extreme case", thinking that's general, and panicking. But this is crazy. We know from the quote above that 0% will be a thing. What we don't know yet is where the #jobs N where will draw the line between 0% and 1%. And then also (though less interesting), other lines from 1 to 2%, and on up. But in any case, I think it is pretty safe to assume that N is going to be, at least, a small integer. (If it's not, then I must revise this opinion. Expect me to revisit the subject when it is announced.)

The current behavior is 50 slots and then a queue; it seems reasonable to me to scale the 0 to 14% over that range, so that there are perhaps 5 jobs per 1% of surcharge. So I am going to make a wild guess that the crowdedness cost will be 0% for zero to four jobs, 1% for five to nine, etc., capped at 14. Where exactly these percentages are does not matter that much; what matters is only just that there are, say, four jobs per station at 0%, nine jobs per station at 1%, and then (less so) for more crowdedness. I take it as given that more than a few percent of surcharge is not sustainable for most industry, whereas zero percent definitely is, and 1% is probably. 2% maybe.

|

| You didn't choose me. |

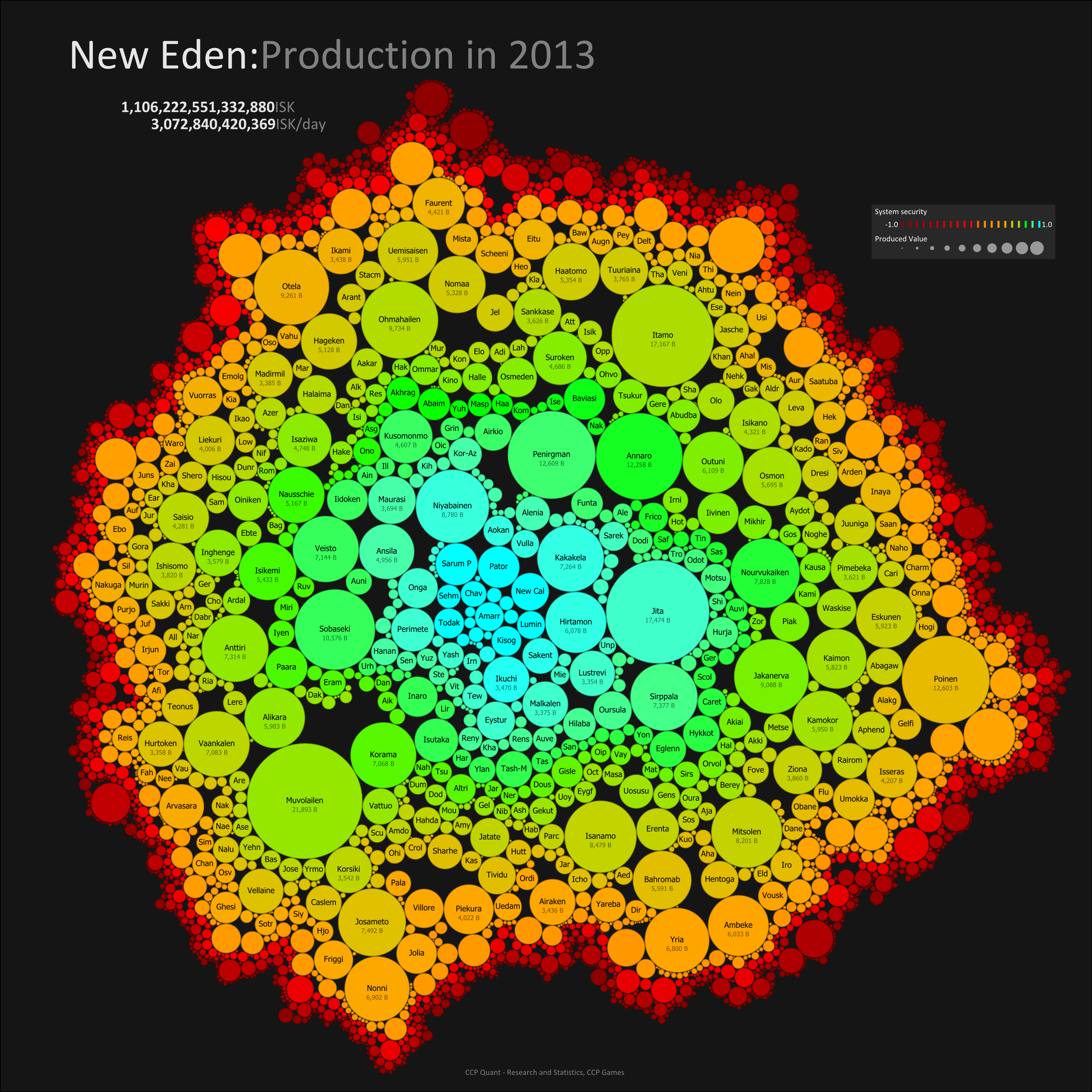

I feel confident that The Forge does the most industry in New Eden, due to the presence of Jita. Remember the dev blog posting Insights into 2013 Production and Destruction. See the picture, and notice all the tiny circles that are blue and green. There are more of them than there are large or even medium blue and green circles.

|

| Production. |

There are currently a lot of empty slots out there; probably more empty ones than filled. Enough for everyone, especially after a substantial amount of the competition moves to POSes or to null.

So, don't panic manufacturers. There will be plenty of room for profit. What we are seeing here is not the evil Nullsec Cartel taking your profit for themselves. We are seeing a leveling of the playing field, so that manufacturing can be done in nullsec and reasonably compete with highsec. You are losing your massive cost advantage, but you are not being made uncompetitive.

That said, there will be some manufacturers that will be better off moving to null, and some better off staying in highsec. This will be a function of transportation cost. Mynnna, though not doing much in his recent blog post to quench the alarm of his critics (here's my comment), did have some useful numbers there on the transportation costs faced by nullsec: "30k isotopes per round trip". Isotopes cost between 700 and 1000 ISK right now, depending on type. And CCP is going to increase fuel requirement for jumping by 50%. So, using a lower end isotope price, we predict transport costs of about 30m ISK for a round trip for a jump freighter. That is a few percent for anything but a very low value load. (To be fair, we must factor in other costs: the capital cost of a jump freighter is one. The effective cost of losses to gank is another. Opportunity cost is also worth mentioning. These are impossible to know.) In any case, the point is that transport costs are significantly higher to and from nullsec than in highsec. Also, there is a balance factor preventing too much industry from moving to null: fuel costs will rise with demand. In highsec, you can autopilot a billion ISK in substantial safety with no fuel cost at all.

So, what we can see is that to the extent nullsec does have a cost advantage in manufacturing proper, industry should be done there first for the things with high value:volume, then decreasingly for things with lower value:volume. The very largest yet low value things, for example T1 ship hulls, will be manufactured in highsec because of the transportation cost advantage. Small, high value stuff, for example most T2 ship parts, will probably move to null. Medium sized stuff will be where the breakeven point is, and might be done in both regions.

Not as convinced about the lack of bounce.

ReplyDeleteThere are no industry "PVP" games that I know of; and this fills a lot (*not all*) of the required gaps.

So, do you like this "teams" thing?

DeleteI'm pretty sure a whole lot of production will move to sov-nullsec, which is getting a decent boost but most of that will be production that was targetting the null-sec markets anyway.

ReplyDeleteThe transport costs will probably eliminate null-sec manufacturing from high-sec materials for high-sec sale for all but the highest isk/volume goods.

T1 ships are an interesting case, it probably makes most sense to manufacture them where they'll be used. For example a perfect Dominix requires just under 14M minerals which is equivalent to around 6000m3 of compressed ore, which is much smaller than its packaged volume of 50000m3.

"T1 ships are an interesting case, it probably makes most sense to manufacture them where they'll be used. For example a perfect Dominix requires just under 14M minerals which is equivalent to around 6000m3 of compressed ore, which is much smaller than its packaged volume of 50000m3."

ReplyDeleteDo you live in null quix? I get the feeling that no one who hasn't done null logistics can evaluate this properly. I.e. I'm a null manufacturer taking advantage of the 10% better refine in null to build cap ships cheaper than lowsec can. I'm shipping jump freighters from high to null filled with compressed minerals every day to feed my chain. What do I fill my JFs with on the return trip? ...dominixes built 15% cheaper than they can be built in high due to the refine buff plus 5% reduction from my amarr outpost? Or do I build a ton of tech2 hulls, enough to fill those return JFs? Even if you do logistics in null now, the shipping patterns will change if more cap production moves to null; as a wh dweller, I don't have any idea how it will play out.

My point about the volumes is you're producing more than 8 times more volume than you're consuming, which limits the amount you can send back efficiently at least. T2 ships would be better.

ReplyDeleteOverall I happen to think that the advantages being dished out to sov-null are probably excessive, but there are massive setup costs to take full advantage of that situation.

It seems a little bit odd that while sov-null has the potential considerable benefits over high-sec, there seems to be little reason to do manufacturing in low-sec or NPC-null over using a backwater high-sec system.

"My point about the volumes is you're producing more than 8 times more volume than you're consuming, which limits the amount you can send back efficiently at least. T2 ships would be better. "

ReplyDeleteYes, I understood your point re: certain t1 ships, but there are thousands of other items being moved back and forth from high to null which you haven't considered. I pointed one out where the m3 volume is the reverse of your situation; my point, which includes your point and moves past it, is that if JFs are on average more full on the high-null trip than they are on the null-high trip, then there is unused space in which one could put thousands of t1 hulls from null to high with no opportunity cost whatsoever.

I am going to make the guess that you haven't seen the blog on the cost of change, or the new one today. they spell out how the costs will work. its not based on number of jobs absolute, but on a square root of the moving average of the percentage of jobs in that system versus all manufacturing... plus a 10% highsec tax. they are trying to screw the highsec players as much as they think they can without them unsubbing. but I think they goofed.

ReplyDeleteRead it. Again, don't panic. The manufacturing charge is going to be that square root thing; this forces people to spread out. But it should work the same for highsec and null, so there is no particular win there. Except, I might point out, that in highsec there are hundreds of systems with manufacturing capability, whereas in null how many Amarr stations are there? I doubt there are anywhere near as many, although I bet many are now being planned.

DeleteAs for the 10%, that's a 10% addition to an already small quantity. That is, if you are smart you will find a less-busy system and you should have a perhaps 3% manufacturing cost. That means 3% of the item's value. The 10% is a multiplier on the 3%; that is, it raises the total cost of the item by .3%. Now, .3% is something, but I bet you can afford it and still compete.

Again, there are costs to manufacturing in null that do not apply to highsec. I.e.: jump fuel, losing the occasional Rhea, etc. This 10% is in part what levels this cost.

first a minor correction to the anon above, its a npc station tax, not highsec specific, but other areas of space are given other ways to mitigate that. second Von you are missing the point. many manufactures are working in margins below 10 % (and if you looked at the cost blog you would have seen that the lowest they currently see on the table being 4%... somewhere in nullsec when their calculations are applied. the highest? 15%, I do support a better isk sink. one of the driving forces behind plex price increase has to be inflation. if people didnt have the isk to pay 700 mil a month than prices wouldnt go there, no matter the demand. so this will squease high volume producers who opperate in tight markets very hard. Price goes up for everyone, but for the nully guys it goes up less.... and if they can work the logistics it could allow them to squease other producers out. that is bad for the general players buying power..... It gets even worse with the teams aspect. large coordinated groups could most likely easily corner the market on these "products" which can grant some pretty substantive cuts to manufacturing cost (through improved efficiency) if they put them in SOV null, something that they can do, it locks out the usefulness to anyone who isnt blued to them. Should manufactures panic? no... just be ready to become renters in null.

ReplyDelete